One of the main reasons the housing market fell apart was sub-prime lending, wherein lenders approved and dispersed loans without regard for whether or not the borrower can repay the loan and interest. The mortgage industry was rife with regulatory loopholes, predatory practices, and continually turned a blind eye toward signals that the market was not nearly as stable as everyone thought.

“A basic characteristic of bubbles is the suspension of disbelief by most participants during the ‘bubble phase.’ There is a failure to recognize that regular market participants and other forms of traders are engaged in a speculative exercise, which is not supported by previous valuation techniques. Also, bubbles are usually identified only in retrospect, after the bubble has burst” (Forbes).

When an economic bubble bursts, it makes the value of the investment plummet. Buyers realize that their purchase was essentially a house of cards and race to unload the tumbling asset. Generally speaking, this is the kiss of death for the product, company, or industry involved.

One of the more devastating bubbles to ever burst was the mortgage market crash, which peaked in 2008 and ultimately took the blame for starting The Great Recession. Within a relatively short period of time, not only did scores of borrowers go into default as variable rate mortgage costs soared, but Wall Street came to the sudden realization that the base of their towering financial architecture was essentially worthless. Due to the enormous role the housing market plays in the United States economy, the government stepped in to try to limit some of the damage by giving certain financial institutions financial assistance -what is commonly known as a “bailout.”

Candace Elliott says, “Economic bubbles rely on the greater fool theory. The people who enter the bubble early may not necessarily believe what they’re buying is useful but what they do think is someone in the future will pay them more for it than what they paid themselves. Somewhere out there is a bigger fool, but at some point, there is the last fool.”

And perhaps that exact point – that most bubbles have investors with little-to-no emotional or ethical stake in the product they are trading – is why student loans have grown into the threatening behemoth they are today. A majority of those who have or are considering getting an advanced degree truly believe that education has limitless intrinsic value. There is a cultural awareness that education is good, degrees are important, and therefore cost isn’t as relevant.

However, the inflated price of higher education is finally defining where value and cost diverge. The decades-old adage that “You go to college, you study, don’t worry so much about how much it costs, it’s going to be worth it in the end” has lost its clout, especially among Millennials and Generation Z students who are saddled with a burden previous generations were not.

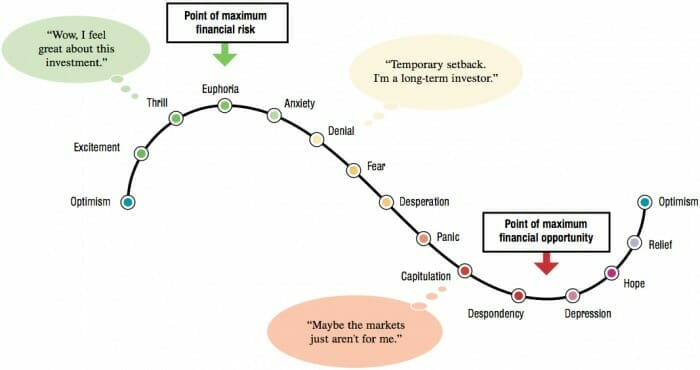

So if the student loan market is truly a bubble, where are we in the predictable cycle? Elliott describes the pattern in this graphic:

If we are to take her at her word, Elliott is sure that educational debt is heading toward a fateful inflection point. “I think the next bubble to burst will be student loans…Lenders started handing out student loans to anyone with a pulse and colleges hiked tuition to obscene amounts.”

Only time will tell whether or not the student loan crisis will morph into yet another large recession, but history seems to indicate that, very simply, we are at the inflection point wherein the value of investing in higher education is no longer worth its cost.

The sad truth is that this issue is not just economic, but has become highly politicized. Easing strain on borrowers, even if it results in financial gain for the nation, is unacceptable to many voters and legislators. No one craves blame, and therefore many are afraid to take a risk by proposing radical change. The bureaucratic bulwark that is the federal government makes change slow and difficult.

But it is easy to forget that there is incredible strength in numbers. When citizens bind together to combat an issue, it becomes far easier to accomplish change. If student loans play a large role in your life or your childrens’ lives, the most helpful thing you can do is to keep the conversation going in your community.

Contact your local and state legislators – they have a huge impact on the price of public school tuition. Don’t rush to take on student debt until you’re really sure what you want to study. And most importantly, stand up for yourself. When it comes to navigating the world of higher education and student loans, you shouldn’t only rely on others to advise you on your educational plan. Do your own research and make informed decisions.

Be your own advocate.