How It All Began

In short, it was innocent. After WWII, the government wanted to help veterans receive an affordable education. Through the GI bill and later the National Defense Education Act, the federal government started investing in citizens by making sure they could get an education if they wished. The government wanted to make sure we had enough intelligent, educated individuals to improve America’s defenses in the Cold War, so it worked with financial institutions to coordinate loans with students, guaranteeing to cover the expenses if a debtor defaulted.

In 1965, the government decided to take over administering student loans directly to students with the passage of the Higher Education Act (HEA). Over the next 20 years, the government would legislate even more access to higher education for low income and female students, including Title IX and expanded access to Pell Grants. The machine seemed to be working well, churning out more college-educated Americans to help our economy and society grow.

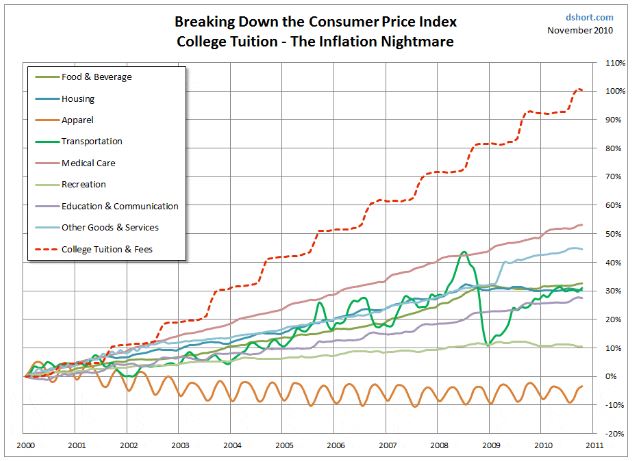

But by the mid-80s, America seemed to notice that there was a growing debt problem. The average student debt per household continued to rise; Between the late 1990s and now, average student debt has risen over 200 percent. Today, one in five American families owe student debt. The average amount per debtor is over $30,000 (Center for Online Education).

Timeline

Scroll left and right to see full timeline

- 1840

Harvard introduces the very first student loan program

- 1944

First federal loans begin via GI Bill

- 1958

National Defense Education Act provides federal loans for all citizens

- 1965

Higher Education Act created Department of Education, which took over administration of student loans

- 1972

Title IX expands student loan rights by outlawing gender descrimination

- 1977

Pell Grants are created for all undergrad students

- 1986

People start noticing that student debt is getting out of hand…

- 1993

Average debt per undergraduate degree reaches $9,000

- 1994

The first Income Contingent Repayment Plan is activated

- 1997

Average debt for an undergraduate degree jumps to $15,000

- 2003

Average debt per undergraduate degree jumps again to $17,500

- 2008

The Great Recession devastates local and global economies

- 2009

The Income-Based Repayment plan goes into effect, requiring a lower percentage of monthly income to be contributed

- 2010

Direct Loans are enacted, cutting out middle men lenders and providing federal loans directly to students

- 2012

Total national student debt reaches $1 trillion and Pay As You Earn (PAYE) repayment plan goes into effect

- 2014

New Income-Based Repayment rules go into effect; Minimum 10% monthly income contribution remains but repayment period shrinks from 25 to 20 years

- 2015

Revised PAYE (REPAYE) allows participation without a partial financial hardship requirement

- 2018

1 in 5 Americans have student debt at an average of $30,000 per debtor

Harvard introduces the very first student loan program

First federal loans begin via GI Bill

National Defense Education Act provides federal loans for all citizens

Higher Education Act created Department of Education, which took over administration of student loans

Title IX expands student loan rights by outlawing gender descrimination

Pell Grants are created for all undergrad students

People start noticing that student debt is getting out of hand…

Average debt per undergraduate degree reaches $9,000

The first Income Contingent Repayment Plan is activated

Average debt for an undergraduate degree jumps to $15,000

Average debt per undergraduate degree jumps again to $17,500

The Great Recession devastates local and global economies

The Income-Based Repayment plan goes into effect, requiring a lower percentage of monthly income to be contributed

Direct Loans are enacted, cutting out middle men lenders and providing federal loans directly to students

Total national student debt reaches $1 trillion and Pay As You Earn (PAYE) repayment plan goes into effect

New Income-Based Repayment rules go into effect; Minimum 10% monthly income contribution remains but repayment period shrinks from 25 to 20 years

Revised PAYE (REPAYE) allows participation without a partial financial hardship requirement

1 in 5 Americans have student debt at an average of $30,000 per debtor

The Great Recession

Although student loan debt continued to increase since the 1980s, it wasn’t until the 2000s that significant legislation was introduced to help mitigate the financial burden of repayment on young Americans. While there were significant improvements to help students prevent default, there was an unforeseen, earth-shattering event that would further upend Americans’ way of life: The Great Recession.

In 2008, the housing market crashed. Years of predatory lending practices, insufficient regulations, and soaring home prices came to a screeching halt when millions of Americans’ mortgage costs surged and droves of accounts went into default. With countless mortgage accounts going unpaid at the same time, the banks were suddenly short billions of dollars. Some banks went under. Others were saved by the federal government in the form of a $700 billion bailout.

While hundreds of thousands of financial sector jobs were suddenly eliminated and the stock market took a nosedive, most bank executives kept their jobs and high salaries due to the influx of government cash. But the most crushing impact of the housing market crash was that the jobs market fell right behind it.

Everyone was feeling squeezed by the economic downturn. Many companies had to downsize or shutter completely. The number of well-paying jobs plummeted, meaning that folks who had lost their homes were also in danger of losing their jobs - or not being able to find one in the first place.

For students completing their education in or around 2008, this set of circumstances severely impacted their ability to jump into their careers and grow their financial portfolios. In a U.S. Department of Education study, students who graduated at the onset of the Great Recession reported significant hardship. Due to the bills associated with their education, 38 percent reported delaying buying a home, 22 percent delayed getting married, 29 percent delayed having children, and 35 percent indicated that they worked more hours than they would like. One out of three respondents indicated they felt unable to balance work and family, and also felt like their jobs were not secure. Even more participants indicated that they felt their compensation was substandard.

Unsurprisingly, student loan defaults increased by 18.9 percent during the Great Recession. Studies would later show that falling home prices hammered the jobs market, which in turn provided students less equity and liquidity. In essence, the housing market crash caused a chain reaction, putting pressure on almost every aspect of our economy.

But thankfully, the government realized that they had to stem the flow of increasing student loan defaults. First, the Student Aid and Fiscal Responsibility Act was introduced, which formally allowed the federal government to loan directly to students without contracting private financial institutions. New income-based repayment plans were introduced such as Pay As You Earn, which reduced the percentage of monthly income that had to be contributed and shortened the repayment period from 25 to 20 years.

Current State of Affairs